The Power of Quick Math: Understanding the Rule of 72

We’ve all heard people talk about “making your money work for you”. But when I first started earning, that phrase felt abstract – almost like a financial jargon. I saved what I could, I invested haphazardly, but never really understood how my money could grow over time.

That changed the day I discovered the Rule of 72. It’s one of the simplest, most powerful concepts in personal finance – and you don’t have to be a math whiz to understand it or to use it. But once you understand it, you’ll see every financial decision in a whole new light.

1. Meet the Rule of 72

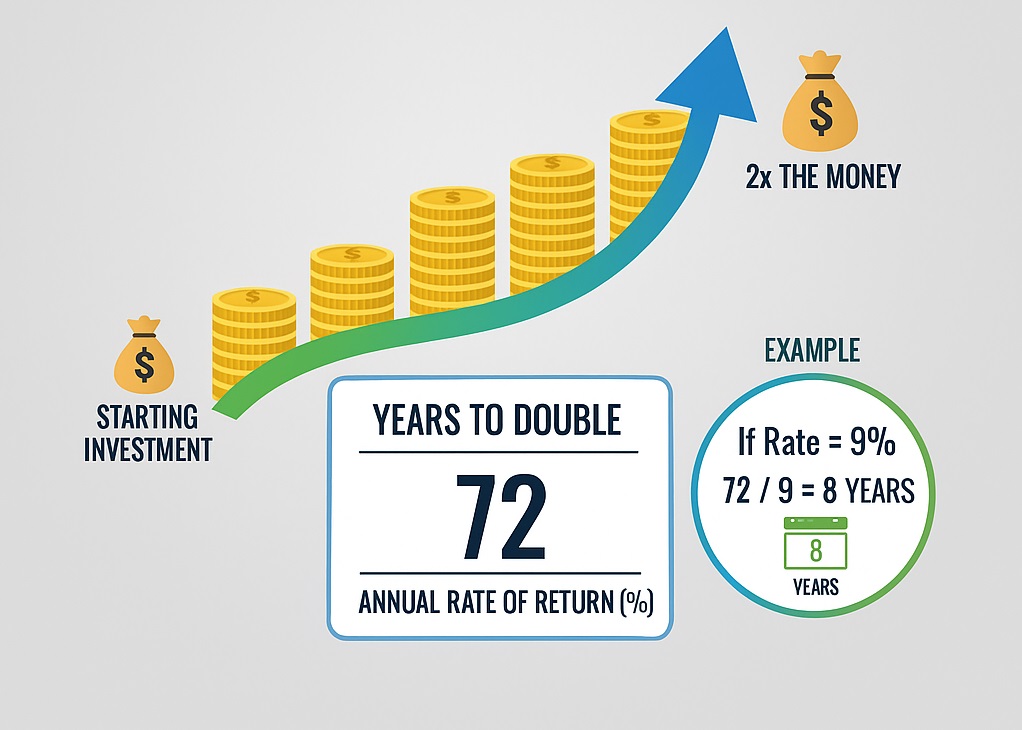

The Rule of 72 is a quick way to estimate how long it takes for your money to double based on a fixed annual rate of return. The math is approximate – but that’s not the point. The math his simple:

Years it takes to double your money = 72 / Annual Rate of Return

For Example:

- If your investment earns 6% per year => It takes 72/6 = 12 years to double.

- If your return is 8% per year => It takes 72/8 = 9 years to double.

- If your return is 2% per year => It takes a whooping 72/2 = 36 years to double

It’s not exact but it’s close enough to help you make smarter, financial decisions.

2. How I learned the hard way

Early in my career, I parked most of savings in a “safe” account – the kind that earns a couple of percent in interest (it wasn’t even 2% then). My balance stayed steady and then grew some – I was already spending less than what I earned. But I didn’t realize how slowly it was actually growing.

One day, a chance conversation with a friend who showed me the Rule of 72 changed me.

“At 2%”, he said, “your money doubles every 36 years. At 8%, it doubles every 9 years. That saves you twenty seven years of your life – without working any harder”. That one sentence hit me like a ton of bricks.

I am an engineer – I knew how compounding works. But I didn’t internalize it – I didn’t have a feel for it. I did the math, and it worked.

I had spent years working hard to increase by income by a few percentage points, yet my money was sitting idle, earning less than inflation. That conversation was the spark that pushed me to learn how investing really works – and it completely changed my relationship with money. This is when I started learning more about money – reading, researching, actioning – and compounding.

3. Why the Rule of 72 matters

Your brain loves simple, memorable shortcuts. That’s why the Rule of 72 sticks. You don’t need complicated math—just a number that shows the power of compounding.

- It reveals the power of compounding: Small difference in return rates create huge differences over time

- It helps you evaluate choices quickly: It gives you a sense of what your returns mean for your future. Let’s face it – most of us can’t do compounding in our heads – or even with a calculator. Rule of 72, while not exact – help us evaluate our choices quickly.

- It shows the cost of inaction: Keeping cash in low-yield accounts may feel safe, but you are quietly losing growth potential every year.

Your brain naturally thinks in linear terms:

100 → 200 → 300 → 400 → 500 -> 600

Straight line. Predictable. Boring.

But compounding doesn’t grow in straight lines. It grows like this:

100 → 200 → 400 → 800 → 1600 -> 3200

Slow at first. Then it explodes.

Of course, it is an extreme example to make a point. Humans underestimate exponential growth. We focus on small short-term gains and miss the magic of compounding. How fast could your money grow if you actually understood this exponential magic?

4. Try it for yourself

Ask yourself:

- How long will it take your savings to double at your current return rate? How long will it take to quadruple?

- What happens if you improve that return by 1%? By 2%? by 4%?

- How does inflation (say, 3%) affect that calculation.

Play with the numbers – the difference might surprise you. Not only that, you could also use the Rule of 72 to get a grasp on your cost of debt as well. Imagine you have a credit card with an 18% interest rate. Your outstanding credit card debt is likely to double in 72/18=4 years. This is how quickly high-interest rate debt can balloon. Minimum payments don’t help your cause much. They are designed to keep you from paying down debt.

Drop in a comment if it surprised you! It sure surprised me when I did this the first time.

5. Use the Rule to Set Goals

Instead of saying, “I want $1 million or a $100,000 someday,” use the Rule of 72 to reverse-engineer your goals:

- Example: You want $100,000 in 15 years.

- Expected return: 8%

- 72 ÷ 8 = 9 → money doubles every 9 years

- How much do you need to start with? Around $25,000. It’ll be $50,000 in 9 years, and $100,000 in 18 years.

Visual, concrete milestones feel achievable. The math is approximate, but your brain is motivated by clarity and predictability.

The Rule of 72 may be simple, but it’s one of those lessons I wish I had learned decades earlier. It’s not just math – it’s a mindset. Once you grasp how time and compounding work together, you start to see money not as something you chase, but as something you grow. When you now hear people saying “Don’t just work for money – make money work for you”, remember they are talking about the compounding effects of money. The Rule of 72 is a wake-up call. When you see how fast interest can double debt, you realize how important it is to pay high-interest balance first. It’s also a good reminder that interest works both ways:

In your favor when you invest.

Against you when you borrow.

What if you could double your money not once, but multiple times before retirement? That’s the magic we want you to eventually unlock.