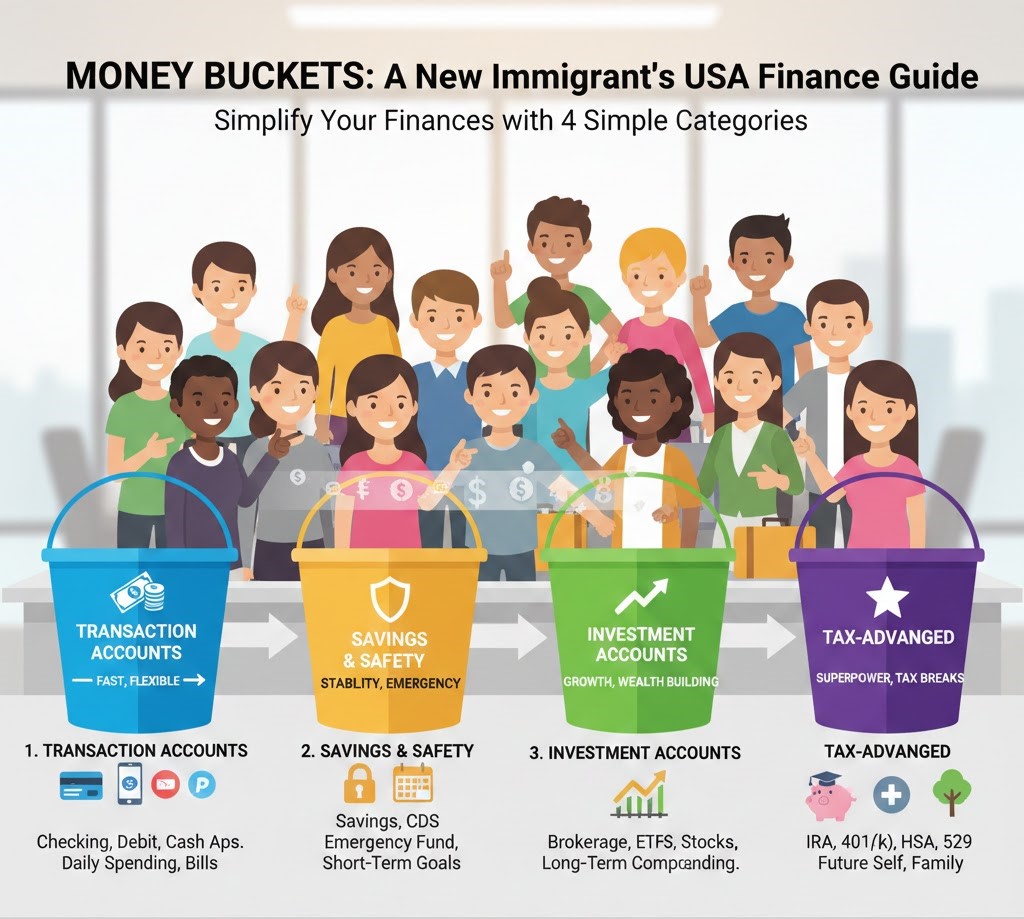

The 4 Types of Accounts You Need to Understand in America

Most people think the U.S. financial system is overloaded with accounts:

Checking.

Savings.

HSA.

IRA.

401(k).

Brokerage.

529.

Business accounts.

Trusts.

CDs.

…And the list somehow never ends.

It gets confusing. This blog post is to help new immigrants to the USA make sense of the accounts here. Instead of discussing each specific account separately, I like to categorize them into four categories to make it easier to handle. You’ll need one or more accounts in each category depending on your stage in life.

Category 1: Transaction Accounts — The “Daily Money” Bucket

This is where your money moves.

It’s cash-in, cash-out. Fast. Flexible. Functional.

What’s included?

- Checking accounts

- Debit-linked cash accounts

- Fintech cash management accounts

- Payment wallets (Venmo, Cash App, PayPal balances)

What they’re designed for:

- Receiving paychecks

- Paying bills

- Daily spending

- Managing cash flow

What they’re NOT designed for:

- Saving

- Growing wealth

This bucket is your money’s home base — but it’s not where your money should live long-term. You want to keep enough to pay your bills – no more than two months of spending – and that’s generous. Remember, most of these accounts do not pay any interest. Your money DOES NOT work for you in these accounts.

Where to open: Any bank or credit union. I’ve had accounts at JP Morgan Chase, PNC Bank etc. but really loved Charles Schwab. They are all big names – and I loved Schwab for they refunded all the ATM fees when traveling abroad. If you do wire transfers often, you may want to check that fees as well. Some banks have minimums, and they would charge a fee unless you hold that minimum – and for that reason I moved away from Chase.

Category 2: Savings & Safety Accounts

This bucket protects your future self from emergencies, surprises, and chaos.

It’s where stability lives.

What’s included?

- Savings accounts

- High-yield savings accounts

- CDs (Certificates of Deposit)

- Money market accounts

What they’re designed for:

- Emergency fund (3–12 months of expenses)

- Short-term goals (travel, car repair, visa fees, moving)

- Safe storage with low risk

What they’re NOT designed for:

- Wealth building

- Beating inflation long-term

This bucket keeps life from derailing when bad news arrives unexpectedly. Most advisors recommend having 3 to 6 months of emergency fund. For those new in the country, and may need additional time to set roots, I would be okay with you having up to 12 months of emergency fund – but remember, it creates a drag on returns.

Where to open: I prefer online banks like Ally Capital One etc. but you could also buy money market funds at Charles Schwab for this purpose. More on this later.

Category 3: Investment Accounts — The “Growth” Bucket

This is the bucket that builds wealth.

If you want financial freedom, this bucket does the heavy lifting.

What’s included?

- Standard brokerage accounts

- Custodial brokerage accounts for kids

- Robo-advisor investment accounts

- Joint investment accounts

What they’re designed for:

- Buying ETFs, stocks, index funds

- Long-term compounding

- Flexible investing with no contribution limits

What they’re NOT designed for:

- Tax reduction

- Ultra-safe short-term saving

This is the bucket where your money stops being lazy and starts working out.

Where to open: I prefer Charles Schwab to have most of my accounts at one place, but would also recommend Vanguard for a lot of low-fee ETFs, or Fidelity. The exact brokerage doesn’t matter much – What matters is you open one.

Category 4: Tax-Advantaged Accounts — The “Superpower” Bucket

This final bucket is where U.S. wealth actually accelerates.

The government gives you tax breaks if you save for big life goals.

What’s included?

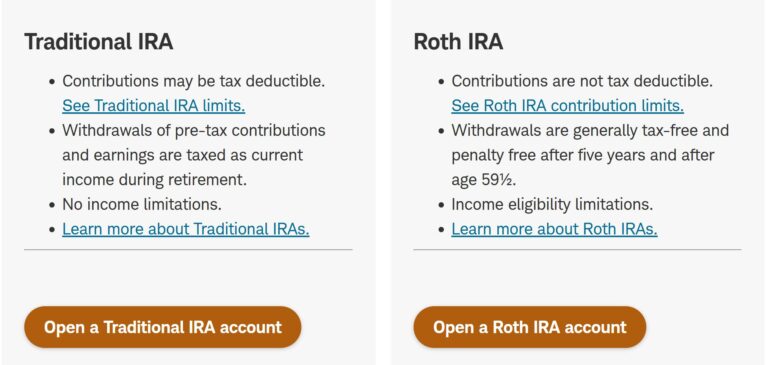

For retirement:

- 401(k)

- Traditional IRA

- Roth IRA

- 403(b), 457(b)

- SEP IRA, Solo 401(k)

For health:

- HSA (triple tax benefits!)

For education:

- 529 plan

- ESA (Education Savings Account)

What they’re designed for:

- Reducing taxes today (Traditional)

- Reducing taxes forever (Roth)

- Growing money tax-free

- Health and education planning

What they’re NOT designed for:

- Frequent withdrawals

- Short-term access

This bucket exists for your future self — and your family’s future selves.

Where to open one: Again, most brokerages (see Category 3) would open one for you. Often times, if you are a W2 earner, you may have one through an employer (and may have limited choices)

The Big Unlock

People don’t struggle because finances are complicated.

They struggle because no one ever taught them the framework.

But now you have it.

Just four categories.

Four buckets.

Four purposes.

Everything in your financial life will likely fit neatly into one of them.

Master these buckets, and you master your money. It’s not an exhaustive list – it’s meant to be a guide for the new comers.