The backdoor Roth IRA: The legal “cheat code” for high-wage W2 earners

If you make too much money for a Roth IRA… you are just about to unlock a secret door the IRS forgot to close.

Most people don’t know it exists.

Even fewer use it.

And almost no one explains it without making you feel like you’re trapped in a tax textbook.

So today, we’re going to open that door.

And peek inside.

And maybe… quietly walk through it.

1. The problem every high wage W2 eventually figures out

You get a raise. You feel good.

Then tax season hits and you discover:

You’re now “too rich” to contribute to a Roth IRA.

The IRS literally says:

“Congrats on earning more… but no tax-free growth for you :)”

Rude.

Because the Roth is the holy grail of retirement accounts:

- money grows tax-free

- withdrawals are tax-free

- no Required Minimum Distributions (an issue that plagues some of the other retirement accounts)

- built for people who want ultimate freedom

But the IRS phases you out once your income crosses a threshold.

Is that really the end? I’m going to cover Roth IRA and other IRAs in a separate blogpost – but if there is something you could do today as a high-income wage earner, I would rank this amongst the simplest.

2. The backdoor nobody mentions, or talks in whispers about

Here’s the twist:

Though the IRS blocks high-income earners from contributing directly…

They never blocked converting money into a Roth.

And that loophole creates the Backdoor Roth IRA:

- Put money into a Traditional IRA.

- Move it to a Roth IRA.

- Boom. You now have money growing tax-free — completely legally.

It’s completely legal. You’re following the rules exactly as written.

Think of it like being told the main entrance is closed…but the side gate is wide

3. Why high-income W-2 earners should care (a lot)

The Roth isn’t just “tax free.” It’s tax protection insurance for your future self.

If you believe you’ll be in a higher bracket later (many W-2 earners will be):

- tax-free growth

- tax-free withdrawals

- tax-free inheritance

- tax-free compounding for 30–40 years

The amount allowed to contribute seems small (if you are a high wage earner), but eventually it compounds. Let’s do a tiny bit of magic math.

If you contribute $6,500/year for 25 years and it grows at 7%:

- Traditional IRA → taxed later

- Roth IRA → ~$442,000 tax-free

That “tax-free” part is what builds generational freedom.

4. It’s going to be quick – The 5-minute step-by-step instructions (spread over two sessions the first time)

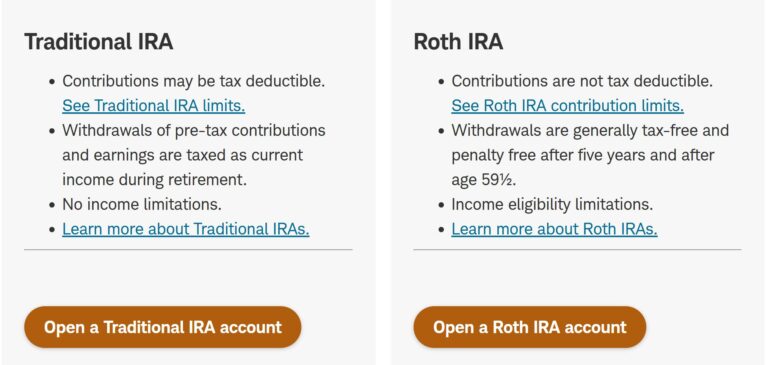

Step 1: Open a Traditional IRA and a Roth IRA.

At Fidelity, Vanguard, Schwab — pick your flavor. If you already have an account at the brokerage, open a traditional IRA/Roth IRA at the same brokerage (keeps the paperwork simpler).

The only real danger: If you already have pre-tax money sitting in any Traditional, SEP, or SIMPLE IRA. Note that this doesn’t include your 401(k) or 403(b) or the like. We are talking about the Individual Retirement accounts. If yours is clean, you have nothing to worry about. If not, there are solutions which I won’t go into because most high earners W2 I know never encountered the problem.

The IRS treats all your IRAs as ONE giant bucket.

Step 2: Put in your contributions (varies by the year) into the Traditional IRA

It’s important you do it to Traditional IRA. Not that there are no income limits on ($7,000 to $8,000 in 2025 depending on your age). Your brokerage in Step 1 will tell you exactly how much you can contribute – so you don’t have to worry! You could transfer funds from your checking or savings account directly into Traditional IRA. Just link it from your brokerage account. At this point, do NOT use your cash to buy any investments in your traditional IRA. A settlement fund, or cash is the way to go.

Important: Do not deduct this contribution if it asks.

You want it as a non-deductible contribution.

Step 3: Transfer your cash from your traditional IRA to your Roth IRA

Wait 7 days and come back. There is no official wait time – but the brokerages put in a hold on your money for up to a week. You could do it sooner if your brokerage allows. The sooner you convert, the sooner you can start growing your wealth tax free. Also, the sooner you convert, less the paperwork. Generally, this is a taxable event – but the taxes are on any growth on top of the $7000 (or $8000) you contributed. Since you contributed only 7 days ago, there likely wasn’t a growth, and there are no taxes to be paid (even though the brokerage would often display a warning.

Step 4: Invest the money

A Roth without investments is a savings account wearing a tuxedo. Put it to work. Buy an index fund if you are unsure. And that’s it!

Step 5: File IRS Form 8606

This happens during tax time. This tells the IRS: “This was non-deductible. Yes, I converted it. Yes, it’s legal. Yes, we’re all good here.”

Did you open yours today? Drop in a comment if you did! Were the instructions useful? Drop in a comment if you got stuck.