The High-Income Tax Trap: Why Your “Safe” Cash Is Getting Eaten Alive (And one ETF That’s Fighting Back)

If you’re a high-income professional—especially someone in a high-tax state—you’ve probably noticed a painful truth: Most “safe” returns are getting decimated by taxes.

Money market funds? Taxed at ordinary income.

Short-term bond funds? Ordinary income.

Treasury bills? Federal tax only, yes—but still ordinary income.

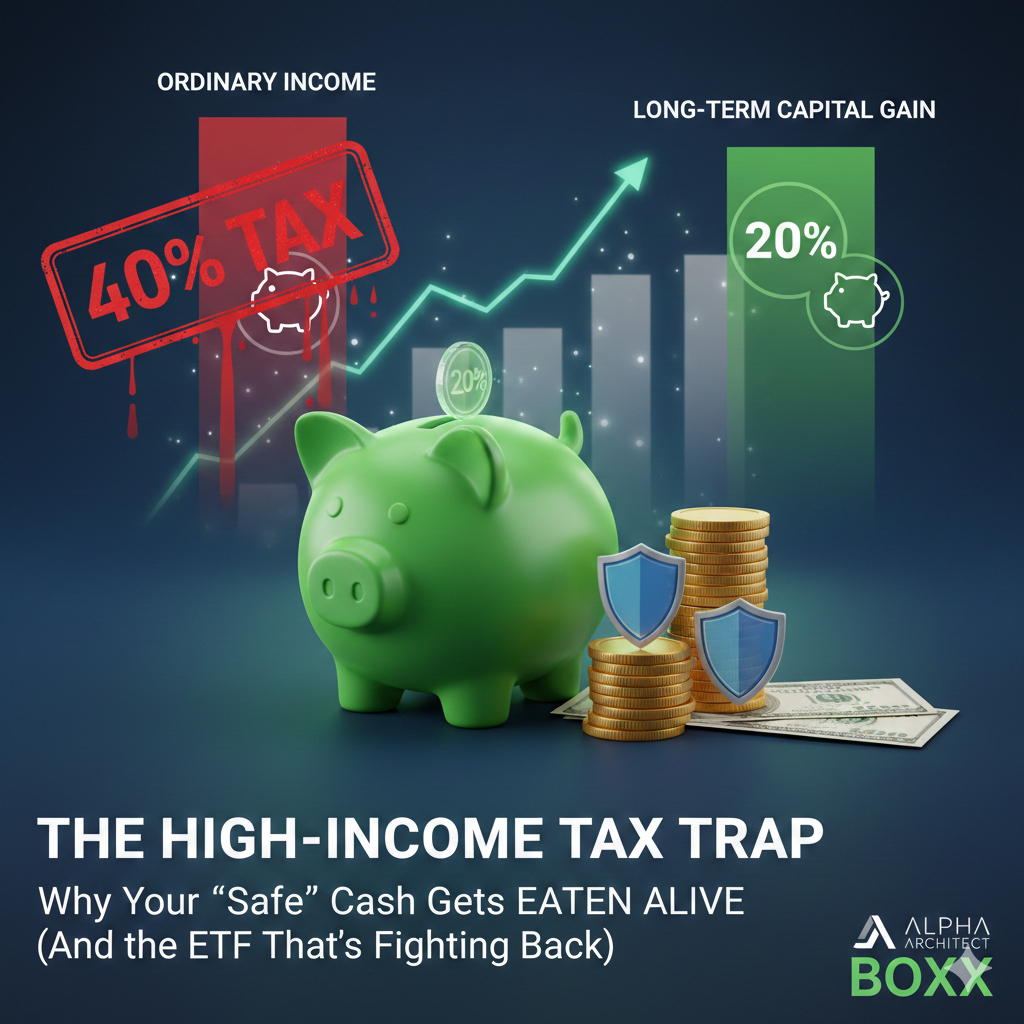

For someone in the 32%–37% federal bracket, plus state taxes and the 3.8% Net Investment Income Tax (NIIT), a 5% yield can lose over 40% to taxes before inflation even shows up.

One specialized approach that has recently gained significant attention is the use of Box-Spread ETFs (like the popular ticker, BOXX).

Disclaimer: This is not a recommendation, and I do not endorse any specific security. The purpose of this post is purely educational. Consult a qualified tax professional before investing in any strategy.

1.What Are Box-Spread ETFs? The Strategy Explained

Box-spread ETFs use a specific options strategy—the box spread—to create a payoff that behaves very similarly to a short-term, low-volatility fixed-income position. Historically, their returns have closely mirrored those of short-term Treasury bills.

The enormous appeal for high earners? The strategy’s return mechanics fundamentally differ from traditional interest income.

Here’s why that matters for your taxable account.

The Tax Alchemy: Turning Ordinary Income into Capital Gains

When you earn a high income, the IRS punishes traditional short-term yields by taxing them at your top marginal rate (up to 37% federally).

Box-spread strategies introduce a critical potential advantage:

1. Capital Gains Characterization (The Core Benefit)

Because these funds generate their income through structured options contracts (box spreads), the underlying return to the fund is characterized as a capital gain, not interest income.

• Traditional Cash: Interest income is taxed annually at your Ordinary Income rate (up to ~37% + NIIT).

• Box-Spread ETF: The fund’s internal gains are not automatically distributed as taxable income. They remain in the fund, causing the share price to appreciate.

2. Tax Deferral and the Magic of 366 Days

This is the financial game-changer for a long-term cash sleeve:

• Deferral: You only pay taxes when you sell the ETF shares, allowing you to defer paying tax for as long as you hold the fund.

• Rate Reduction: If you hold the ETF for more than one year and a day (366 days), the entire accumulated gain is potentially taxed at the much lower Long-Term Capital Gains (LTCG) rate—which caps out at 20% (plus NIIT).

Translation: You are essentially converting a high-taxed annual income stream (up to 37%+) into a low-taxed, one-time deferred gain (up to 20%).

3. The Tax Efficiency of the ETF Structure

Even though these strategies involve frequent options activity, the regulated ETF structure makes them remarkably tax-friendly:

• No Annual Distributions: ETFs can use a mechanism called “in-kind redemptions” to prevent capital gains from being distributed to shareholders.

• You Control the Tax Event: You, the investor, decide when to sell and realize the gain, giving you complete control over the tax timing.

4. Who Might Explore This Strategy?

Box-spread ETFs are tools—not magic, and not universally superior. They are specifically designed for a certain type of investor and situation.

✓ High-Income Professionals with Large Taxable Accounts

This is the ideal use case. If you have significant cash or low-duration fixed income in a brokerage account that is throwing off a lot of taxable ordinary income, this strategy is worth investigating.

✓ Investors Who Already Max Out Tax-Advantaged Accounts

Once you’ve fully funded your 401(k), HSA, Backdoor Roth, and any other qualified plan, your taxable brokerage account becomes your main battlefield for tax efficiency. This is a tool for that battlefield.

✓ Those Seeking Short Duration without Bond Tax Drag

You want to avoid the volatility and interest rate risk of long-term bonds, but you don’t want the ordinary income tax of short-term bond funds. The box spread is mathematically defined to avoid duration risk without generating traditional bond income.

Essential Cautions & Risks

Before diving in, you must understand the risks and ongoing debates surrounding this strategy:

Regulatory Risk: The IRS has anti-abuse rules (Sections 1258 and 1092) designed to prevent “converting” interest-equivalent income into capital gains. While the funds operate today, the ultimate tax treatment is not guaranteed and could be challenged in the future.

Not completely Risk Free: These are not FDIC-insured, are not cash equivalents, and are not guaranteed. They are subject to issuer risk, counterparty risk, and general market risk (though volatility is designed to be minimal)

Final Thoughts: Tax Efficiency Is Your Best Return

As a financial coach, my goal is to help you keep more of what you earn. When money market yields are high, the cost of tax inefficiency is at its peak.

Box-spread strategies offer:

• The potential for massive tax deferral.

• The potential for lower long-term capital gains rates.

• Short-duration exposure with low volatility.

In the end, the right vehicle depends on your personal financial architecture. Box-spread ETFs are simply one more powerful—and complex—tool high-income households should understand as they fight the good fight against tax drag. I personally allocate a proportion of what I would otherwise keep in a high yielding savings account to buy BOXX.

Which of your current accounts is creating the most unnecessary tax drag? Let me know in the comments!